Running a small business often means juggling resources and making financial decisions that will shape your company’s growth for years. One of the most pressing questions many small business owners face is how to secure the equipment, vehicles, or even office space needed to keep things running smoothly—without overburdening cash flow. Leasing becomes an attractive option, but the real choice lies in which kind of lease to pursue: finance lease or operating lease.

The decision isn’t as straightforward as it seems. Each has unique implications for costs, taxes, accounting treatment, and long-term business flexibility. Understanding these nuances can help a small business not only avoid costly mistakes but also create a strategy that aligns with growth goals. So lets take a look at a finance vs operating lease and what works best for small and upcoming businesses.

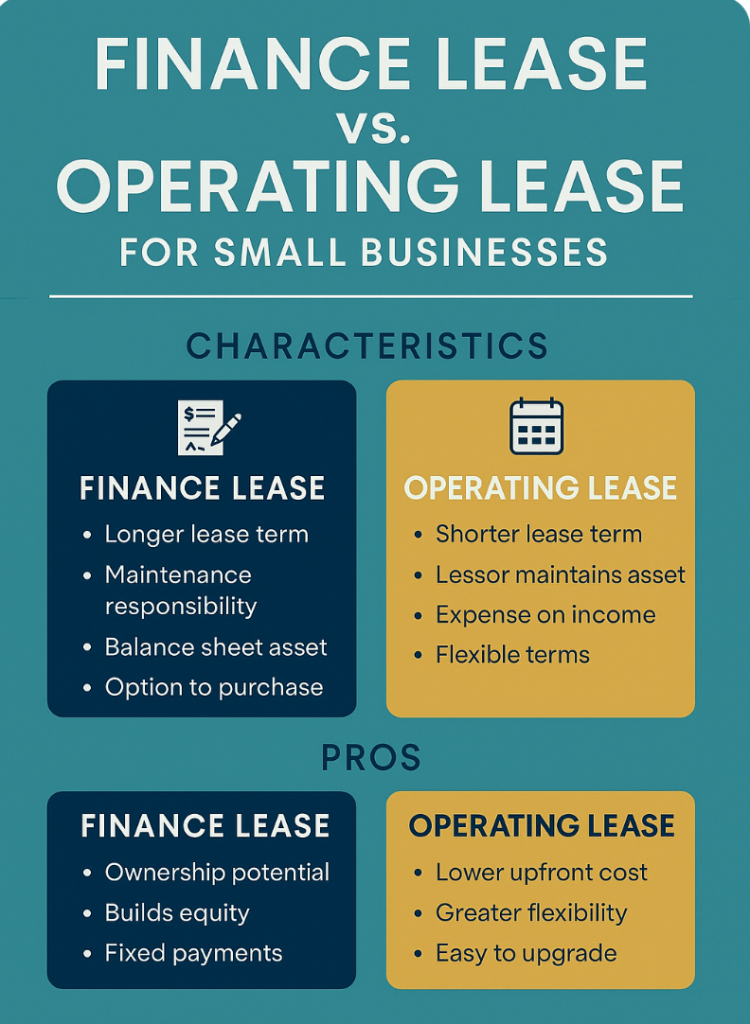

What Is a Finance Lease?

A finance lease—sometimes called a capital lease—is essentially a way of financing the purchase of an asset without paying for it outright. Think of it as renting something long-term, but with the intent that you’ll own it (or at least bear most of the risks and rewards of ownership) by the end of the contract.

Key characteristics include:

- The lease term often covers most of the asset’s useful life.

- The business assumes responsibility for maintenance and insurance.

- At the end of the lease, you may have the option to buy the asset for a nominal fee.

- It appears on your balance sheet as both an asset and a liability.

For small businesses, a finance lease works well for equipment or property you expect to use long term and don’t want to replace frequently—like delivery vans, specialized machinery, or office furniture.

What Is an Operating Lease?

An operating lease is closer to a rental agreement. The business pays to use the asset for a shorter period, typically less than the asset’s economic life, and returns it at the end of the contract.

Characteristics include:

- Shorter lease terms (often 1–5 years).

- Maintenance is often handled by the lessor, not the business.

- The asset does not appear on your balance sheet in the same way a finance lease does.

- Payments are treated as operating expenses, fully deductible for tax purposes.

For small businesses, operating leases are appealing if you want flexibility, frequently upgrade equipment, or don’t want to commit to long-term ownership.

Finance Lease vs. Operating Lease: Accounting Impact

The accounting treatment of each lease type is one of the most significant differences—and something small businesses can’t afford to ignore.

- Finance Lease: Appears on the balance sheet, increasing both assets and liabilities. It can affect debt ratios and financial metrics, but it also builds equity in the asset.

- Operating Lease: Traditionally kept off the balance sheet, it’s treated as an expense. However, under newer accounting standards (like ASC 842 and IFRS 16), many operating leases must also be recognized as liabilities if they’re longer than 12 months.

This distinction matters because lenders and investors often scrutinize balance sheets. A finance lease might make your business look more leveraged, while an operating lease keeps things simpler.

Tax Benefits

Both lease types can provide tax benefits, but in different ways.

- With a finance lease, you can claim depreciation on the asset and deduct the interest portion of lease payments.

- With an operating lease, the entire lease payment is deductible as a business expense.

For businesses with fluctuating profits, operating leases can provide a more straightforward and immediate deduction, while finance leases spread benefits over time.

Which Lease Is Better for Cash Flow?

Cash flow is the lifeblood of small businesses.

- Finance leases often involve higher monthly payments, since you’re effectively buying the asset over time. This can strain short-term cash flow but gives you long-term ownership.

- Operating leases usually have lower payments, making them easier to fit into tight budgets. The trade-off is that you won’t own the asset at the end of the term.

For young firms or those in industries with rapidly changing technology (like IT), operating leases often provide more flexibility without tying up capital.

Long-Term Considerations

Choosing between a finance lease and an operating lease isn’t just about today’s payments—it’s about where you see your business in five or ten years.

- Finance Lease Pros:

- You eventually own the asset, which can be sold or continued in use.

- It can build equity in high-value equipment.

- Better for businesses that need stability and won’t replace equipment often.

- Operating Lease Pros:

- Flexibility to upgrade equipment or vehicles more frequently.

- Lower upfront and monthly costs.

- Less responsibility for maintenance.

The question to ask yourself: Do I want flexibility and agility, or stability and ownership?

A Practical Example

Let’s say you run a small logistics company in Texas. You need five delivery vans.

- With a finance lease, you’ll have higher monthly payments, but after five years, you’ll own the vans outright. That makes sense if you plan to keep them running for eight to ten years.

- With an operating lease, your payments are lower, but after three years, you’ll return the vans and likely lease newer models. This could be a better choice if you want fuel-efficient, reliable vehicles without the hassle of long-term maintenance.

Both options are valid—but your business model will determine which is smarter.

Key Factors Small Businesses Should Consider

When deciding, weigh these elements:

- Industry: Fast-moving industries benefit from operating leases; stable industries may prefer finance leases.

- Asset Type: Technology (computers, servers) is better suited for operating leases. Long-lived assets (buildings, heavy machinery) often fit better with finance leases.

- Growth Plans: If you expect rapid growth, maintaining flexibility with operating leases may be wise.

- Cash Flow: Tight budgets often make operating leases the only realistic option.

- Accounting and Tax Strategy: Work with your accountant to see which lease type optimizes your tax and balance sheet goals.

Hybrid Strategies

Some businesses adopt a mix: using finance leases for core, long-term assets while relying on operating leases for fast-changing or secondary needs. This hybrid approach provides both stability and flexibility.

For example, a dental practice might finance lease the building’s dental chairs and X-ray machines but operate lease office computers that need replacing every few years.

The Verdict: Which Is Usually Better Long Term?

For small businesses focused on long-term stability and asset building, finance leases often provide the most value. They create ownership, prevent you from paying endlessly for rentals, and can strengthen the business’s asset base.

However, for businesses prioritizing flexibility, low upfront costs, and adaptability, operating leases usually win. In fast-changing industries or during the early growth stages, being able to upgrade or pivot without long-term obligations is invaluable.

In truth, there’s no universal winner. The “better” option depends on your industry, cash flow, and growth ambitions. The smartest small businesses weigh the trade-offs carefully, often blending both approaches.

Final Thoughts

Small business success is built on smart financial decisions. Leasing, whether finance or operating, is more than a way to avoid upfront costs—it’s a strategic tool. A finance lease can anchor your business with valuable assets, while an operating lease can keep you nimble in a competitive market.

The key is alignment: choose the lease type that supports—not constrains—your vision for the future. For some, that means building equity through ownership; for others, it means keeping doors open for rapid change.

Either way, understanding the differences empowers you to negotiate better terms, protect your cash flow, and ensure that every lease signed is another step toward sustainable growth.